“Il mondo si sta muovendo rapidamente verso un assetto multipolare. Questo, in molti modi, è positivo. Porta nuove opportunità di giustizia ed equilibrio nelle relazioni internazionali. Ma il multipolarismo, da solo, non può garantire la pace.” — António Guterres, Segretario Generale ONU, 2023

Geopolitica: i conflitti si congelano

Nel 2026 i principali conflitti globali non termineranno con vittorie schiaccianti, ma con tregue e congelamenti. In Ucraina si arriverà a un cessate-il-fuoco di fatto: Mosca manterrà territori occupati, Kiev resterà sovrana con il sostegno occidentale. A Gaza un cessate-il-fuoco multilaterale, sostenuto da Stati Uniti, Egitto, Qatar e ONU, stabilizzerà la Striscia. La crisi di Taiwan resterà contenuta: Pechino continuerà con pressioni militari simboliche, senza invadere. In Africa il Sahel sarà diviso in nuove sfere di influenza, mentre in Congo la tregua mediata dal Qatar ridurrà un conflitto decennale. Il Venezuela sarà reintegrato nel mercato globale, e in Medio Oriente la distensione tra Arabia Saudita e Iran resisterà, aprendo a nuovi accordi. Il filo rosso sarà chiaro: i conflitti resteranno irrisolti, ma verranno incanalati in un equilibrio multipolare che eviterà escalation globali.

Finanza: il mosaico monetario

La de-dollarizzazione accelererà. Sempre più scambi energetici e commerciali avverranno in yuan, rupie o rial. Il dollaro resterà centrale ma non più egemonico. Accanto ad esso emergerà un sistema policentrico fatto di dollaro, yuan, euro, oro e Bitcoin. Gli investitori privilegeranno oro, bond a breve termine, mercati emergenti e Bitcoin come asset complementare. Le borse occidentali cresceranno moderatamente, mentre i listini asiatici guideranno i flussi globali.

Tecnologia e spazio: frammentazione gestita

Il 2026 confermerà la splinternet: Internet sarà diviso in blocchi regionali, con la Cina e la Russia sempre più chiuse e l’Occidente a difendere un web aperto. I paesi emergenti adotteranno modelli ibridi, tra controllo e apertura.

L’intelligenza artificiale raggiungerà livelli inediti di creatività e autonomia. Crescerà la pressione per un trattato internazionale che limiti le armi autonome, con l’ONU impegnata a proporre un’agenzia di controllo simile all’AIEA.

Nello spazio, la competizione sarà più politica e tecnologica che materiale. Gli Stati Uniti punteranno a riportare astronauti sulla Luna con Artemis, mentre la Cina intensificherà i preparativi per missioni con equipaggio entro il 2030. Musk e Bezos continueranno a giocare un ruolo di acceleratori, con Starship e Blue Origin pronti a ridurre i costi di accesso allo spazio. Non nasceranno basi permanenti, ma il 2026 segnerà il ritorno della Luna e di Marte al centro dell’immaginario geopolitico multipolare.

Società e lavoro: dopo la crisi

Con la fine dell’inflazione bellica i consumi torneranno a crescere. Le nuove classi medie di Asia e Africa guideranno la domanda globale. Il lavoro sarà trasformato dall’IA e nasceranno nuove figure professionali. In Europa e Nord America sperimentazioni di reddito di base universale compenseranno l’impatto sociale. La Cyber Generation userà la propria forza digitale per imporre priorità di pace, giustizia e sostenibilità.

I miliardari come nuovo polo di potere

Il 2026 mostrerà come i miliardari tecnologici siano ormai un terzo polo geopolitico. Elon Musk, con infrastrutture come Starlink, influenzerà scelte di sicurezza. Jeff Bezos investirà in spazio e media come attore statale. I grandi fondi globali orienteranno transizioni energetiche e mercati come veri super-ministeri. Questi attori avranno interesse diretto nella stabilità: la loro influenza sarà un fattore determinante verso la Multipolar Peace.

2027–2028: pace fragile o coesistenza stabile?

Il rischio di nuove escalation rimarrà: cambi di leadership, shock climatici o crisi interne potrebbero riaccendere tensioni. Ma se gli accordi del 2026 verranno consolidati, nascerà una fase di coesistenza multipolare stabile: competizione economica e tecnologica, meno guerre dirette. Il 2026 sarà ricordato come l’anno in cui il mondo avrà compreso che la pace non nasce dall’egemonia di uno solo, ma dall’equilibrio di molti.

Questo testo è una libera riflessione a scopo di studio prospettico e non rappresenta verità assolute né consigli operativi. Le considerazioni espresse valgono alla data di pubblicazione (agosto 2025) e possono mutare con l’evolversi degli eventi

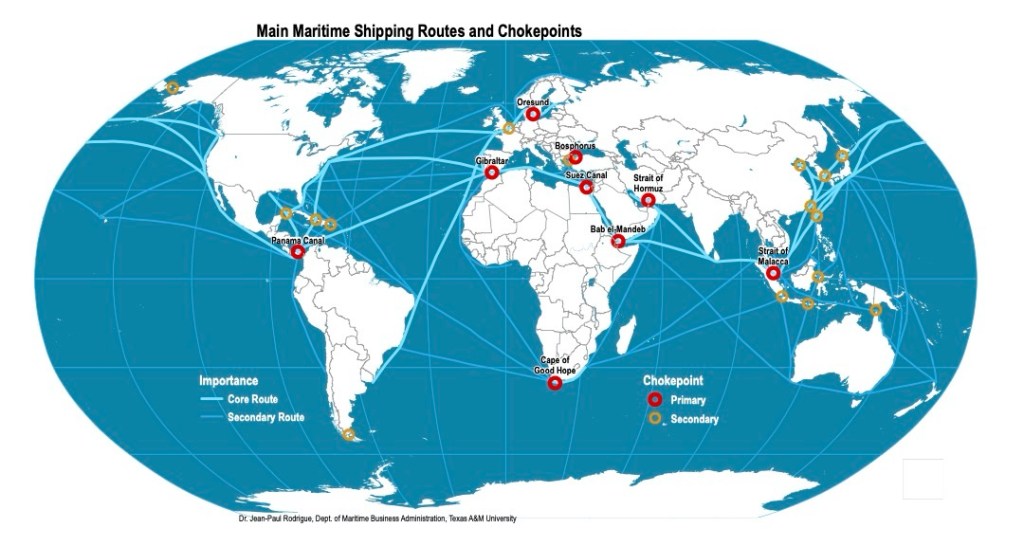

To understand what is happening in the world today, we must start from a simple yet powerful idea: globalization is, above all, control of the seas. It is not just about trade, technology, or financial flows, but about the ability to ensure—or block—the free transit of goods and energy along the world’s major maritime routes.

History teaches this clearly. Every dominant empire has built its power through strategic control of the waters: Rome unified the Mediterranean, turning it into an internal lake—“mare nostrum”; the British Empire established naval bases across the globe, from the Suez Canal to Singapore; and finally, the United States, which since the end of World War II has dominated the oceans, sustaining the liberal global order with an unrivaled navy.

But no hegemony, however solid, remains unchallenged forever.

⸻

The American Empire in a Phase of Fatigue

Today, the United States still appears formally dominant, but less capable of exercising its authority unopposed. It is not so much a military weakness as a perceptual fatigue—a loss of confidence, both domestically and internationally, that creates room for other powers to rise. This perception—and the reality that follows—carries tremendous weight: in international relations, the perception of strength is already strength, just as the perception of weakness is already an invitation to challenge.

It is into this vacuum that determined actors are stepping: China, Russia, Turkey, and Iran, each carrying a worldview and, often, a historical empire to which they appeal to legitimize their expansion.

⸻

The Return of Empires

It is no coincidence that these emerging powers explicitly reference history. The United States sees itself as the heir to the British Empire—not just linguistically and culturally, but as a global maritime guardian. China, with its millennia-old civilization, has revived the Belt and Road Initiative, not only by land but especially by sea, building strategic ports from Asia to Africa. Russia aims to reconstruct a post-Soviet sphere of influence, supported by a czarist and Orthodox vision. Turkey, nostalgic for Ottoman glory, is now very active in the Eastern Mediterranean and Syria. And Iran presents itself as the spiritual and geopolitical heir of the Persian Empire, with a regional agenda aimed at shaping the broader Middle East.

These actors are not merely competing symbolically. They have concrete goals: regional influence, market access, energy control, and military presence in key global hotspots. And all of these goals, inevitably, pass through the sea.

⸻

The New Map of Power: Strategic Straits

If the seas are the arteries of globalization, the straits are its vital points. They are narrow spaces where everything passes—and where everything can be blocked. This makes them the true fault lines of modern geopolitics.

The Suez Canal links Europe to Asia; even a partial closure causes immediate price shocks globally. The Bosporus and Dardanelles, controlled by Turkey, are essential for Russia and the entire Black Sea region. The Strait of Gibraltar remains a critical gateway to the Mediterranean. The Bab-el-Mandeb, between Yemen and the Horn of Africa, connects the Red Sea to the Indian Ocean, with direct consequences for European energy security.

The Strait of Hormuz may be the most delicate of all: nearly one-third of the world’s oil passes through it. Every Iran–U.S. tension plays out here as well. The Strait of Malacca, by contrast, is vital for China: a major portion of its trade flows through it, making it extremely sensitive in any potential conflict.

Further north, the Bering Strait—between Alaska and Siberia—gains relevance, not only symbolically as a frontier between two superpowers but also strategically in a world where Arctic routes are becoming navigable. Finally, the Taiwan Strait is now the epicenter of global tension: a geopolitical flashpoint where economic, technological, and military interests intersect.

⸻

Ongoing Wars: Symptoms of a Reordered World

Each current conflict can be interpreted as an attempt to redefine the global order. The war in Ukraine is not simply a clash between two states but a Russian challenge to NATO expansion and its own post-Soviet marginalization. In Syria, Turkey intervenes to control Kurdish dynamics and safeguard its regional influence. In Gaza, Iran strengthens its role in the anti-Israel axis and within the broader Middle Eastern theater.

Tensions around Taiwan may be the most dangerous: China claims the island as its own, and any attempt at reunification—even by force—would mark a critical turning point in its standoff with the United States. For now, Washington responds economically, using tariffs and technological restrictions in an effort to slow Chinese military and digital development without triggering open warfare.

⸻

A World Reassembling: Between Power, Narrative, and Perception

The Taiwan case is more than a territorial dispute. It is the symbolic center of a much broader challenge: that between two worldviews. On one side, a liberal, multilateral order led by the United States, which has provided decades of maritime stability and commercial growth. On the other, a new multipolar order in which emerging powers demand more space, influence, and control over strategic routes and global flows.

But the real battle is not just over who rules, but how reality is told and perceived. Narrative power matters as much as military power. China and Russia are not only challenging U.S. dominance at sea—they are also attacking its moral, cultural, and economic primacy. In this sense, the conflict also plays out in the minds of public opinion and in the diplomacy of neutral or non-aligned nations.

Globalization is not over—but it is changing its face. From an integrated, Western-led system, we are shifting to a more fragmented mosaic, where each power seeks to defend its sphere of influence, even at the expense of global cooperation. In this context, seas, straits, ports, and canals become arenas of strategic competition once again. It is the return of infrastructure geopolitics and chokepoint diplomacy.

⸻

Economic Impacts and New Financial Strategies

This new global context does not remain confined to diplomacy or armed conflict: it has direct and deep effects on financial markets. Wars, sanctions, naval blockades, geopolitical realignments, and trade tensions make future scenarios increasingly uncertain and volatile.

The consequences are visible across at least three dimensions:

1. Structural inflation: supply chain disruptions and the race for strategic self-sufficiency (in energy, tech, raw materials) are driving up global costs.

2. Market volatility: instability is growing—not only in countries directly involved in conflicts but at a systemic level.

3. End of the linear paradigm: predictable, steady growth models are becoming obsolete, prompting a fundamental rethink of risk itself.

In this setting, traditional passive investment strategies—like recurring index-based plans (e.g., PACs)—are showing their limitations. While still valid for long-term retail investors, they no longer suffice for those seeking resilience in a multipolar, high-entropy world.

Thus, we are witnessing a return—or rather a reinforcement—of more dynamic and adaptive approaches, such as those labeled “Absolute Return” strategies. These are not brand new: they have existed in institutional portfolios for decades. But their relevance increases in scenarios where the goal is not to beat the market, but to protect capital across all market phases.

Absolute Return strategies may include:

• Long/short instruments, which can profit in both rising and falling markets;

• Active hedging against inflation, volatility, or geopolitical shocks;

• Selective exposure to currencies, commodities, or assets uncorrelated with traditional markets.

Additionally, multi-strategy models are gaining traction—blending quantitative algorithms, macroeconomic analysis, and geopolitical intelligence—to deliver stable, non-cyclical returns.

In short: in a world where global powers are contesting control of the seas, investors must redraw their mental maps. Sailing blind is no longer an option, nor is following routes set by past textbooks. A new compass is needed—one capable of navigating not just quarterly earnings and equity indices, but the Strait of Hormuz, tech tariffs, and capital flows chasing the next strategic alliance.

To understand what is happening in the world today, we must start from a simple yet powerful idea: globalization is, above all, control of the seas. It is not just about trade, technology, or financial flows, but about the ability to ensure—or block—the free transit of goods and energy along the world’s major maritime routes.

History teaches this clearly. Every dominant empire has built its power through strategic control of the waters: Rome unified the Mediterranean, turning it into an internal lake—“mare nostrum”; the British Empire established naval bases across the globe, from the Suez Canal to Singapore; and finally, the United States, which since the end of World War II has dominated the oceans, sustaining the liberal global order with an unrivaled navy.

But no hegemony, however solid, remains unchallenged forever.

⸻

The American Empire in a Phase of Fatigue

Today, the United States still appears formally dominant, but less capable of exercising its authority unopposed. It is not so much a military weakness as a perceptual fatigue—a loss of confidence, both domestically and internationally, that creates room for other powers to rise. This perception—and the reality that follows—carries tremendous weight: in international relations, the perception of strength is already strength, just as the perception of weakness is already an invitation to challenge.

It is into this vacuum that determined actors are stepping: China, Russia, Turkey, and Iran, each carrying a worldview and, often, a historical empire to which they appeal to legitimize their expansion.

⸻

The Return of Empires

It is no coincidence that these emerging powers explicitly reference history. The United States sees itself as the heir to the British Empire—not just linguistically and culturally, but as a global maritime guardian. China, with its millennia-old civilization, has revived the Belt and Road Initiative, not only by land but especially by sea, building strategic ports from Asia to Africa. Russia aims to reconstruct a post-Soviet sphere of influence, supported by a czarist and Orthodox vision. Turkey, nostalgic for Ottoman glory, is now very active in the Eastern Mediterranean and Syria. And Iran presents itself as the spiritual and geopolitical heir of the Persian Empire, with a regional agenda aimed at shaping the broader Middle East.

These actors are not merely competing symbolically. They have concrete goals: regional influence, market access, energy control, and military presence in key global hotspots. And all of these goals, inevitably, pass through the sea.

⸻

The New Map of Power: Strategic Straits

If the seas are the arteries of globalization, the straits are its vital points. They are narrow spaces where everything passes—and where everything can be blocked. This makes them the true fault lines of modern geopolitics.

The Suez Canal links Europe to Asia; even a partial closure causes immediate price shocks globally. The Bosporus and Dardanelles, controlled by Turkey, are essential for Russia and the entire Black Sea region. The Strait of Gibraltar remains a critical gateway to the Mediterranean. The Bab-el-Mandeb, between Yemen and the Horn of Africa, connects the Red Sea to the Indian Ocean, with direct consequences for European energy security.

The Strait of Hormuz may be the most delicate of all: nearly one-third of the world’s oil passes through it. Every Iran–U.S. tension plays out here as well. The Strait of Malacca, by contrast, is vital for China: a major portion of its trade flows through it, making it extremely sensitive in any potential conflict.

Further north, the Bering Strait—between Alaska and Siberia—gains relevance, not only symbolically as a frontier between two superpowers but also strategically in a world where Arctic routes are becoming navigable. Finally, the Taiwan Strait is now the epicenter of global tension: a geopolitical flashpoint where economic, technological, and military interests intersect.

⸻

Ongoing Wars: Symptoms of a Reordered World

Each current conflict can be interpreted as an attempt to redefine the global order. The war in Ukraine is not simply a clash between two states but a Russian challenge to NATO expansion and its own post-Soviet marginalization. In Syria, Turkey intervenes to control Kurdish dynamics and safeguard its regional influence. In Gaza, Iran strengthens its role in the anti-Israel axis and within the broader Middle Eastern theater.

Tensions around Taiwan may be the most dangerous: China claims the island as its own, and any attempt at reunification—even by force—would mark a critical turning point in its standoff with the United States. For now, Washington responds economically, using tariffs and technological restrictions in an effort to slow Chinese military and digital development without triggering open warfare.

⸻

A World Reassembling: Between Power, Narrative, and Perception

The Taiwan case is more than a territorial dispute. It is the symbolic center of a much broader challenge: that between two worldviews. On one side, a liberal, multilateral order led by the United States, which has provided decades of maritime stability and commercial growth. On the other, a new multipolar order in which emerging powers demand more space, influence, and control over strategic routes and global flows.

But the real battle is not just over who rules, but how reality is told and perceived. Narrative power matters as much as military power. China and Russia are not only challenging U.S. dominance at sea—they are also attacking its moral, cultural, and economic primacy. In this sense, the conflict also plays out in the minds of public opinion and in the diplomacy of neutral or non-aligned nations.

Globalization is not over—but it is changing its face. From an integrated, Western-led system, we are shifting to a more fragmented mosaic, where each power seeks to defend its sphere of influence, even at the expense of global cooperation. In this context, seas, straits, ports, and canals become arenas of strategic competition once again. It is the return of infrastructure geopolitics and chokepoint diplomacy.

⸻

Economic Impacts and New Financial Strategies

This new global context does not remain confined to diplomacy or armed conflict: it has direct and deep effects on financial markets. Wars, sanctions, naval blockades, geopolitical realignments, and trade tensions make future scenarios increasingly uncertain and volatile.

The consequences are visible across at least three dimensions:

1. Structural inflation: supply chain disruptions and the race for strategic self-sufficiency (in energy, tech, raw materials) are driving up global costs.

2. Market volatility: instability is growing—not only in countries directly involved in conflicts but at a systemic level.

3. End of the linear paradigm: predictable, steady growth models are becoming obsolete, prompting a fundamental rethink of risk itself.

In this setting, traditional passive investment strategies—like recurring index-based plans (e.g., PACs)—are showing their limitations. While still valid for long-term retail investors, they no longer suffice for those seeking resilience in a multipolar, high-entropy world.

Thus, we are witnessing a return—or rather a reinforcement—of more dynamic and adaptive approaches, such as those labeled “Absolute Return” strategies. These are not brand new: they have existed in institutional portfolios for decades. But their relevance increases in scenarios where the goal is not to beat the market, but to protect capital across all market phases.

Absolute Return strategies may include:

• Long/short instruments, which can profit in both rising and falling markets;

• Active hedging against inflation, volatility, or geopolitical shocks;

• Selective exposure to currencies, commodities, or assets uncorrelated with traditional markets.

Additionally, multi-strategy models are gaining traction—blending quantitative algorithms, macroeconomic analysis, and geopolitical intelligence—to deliver stable, non-cyclical returns.

In short: in a world where global powers are contesting control of the seas, investors must redraw their mental maps. Sailing blind is no longer an option, nor is following routes set by past textbooks. A new compass is needed—one capable of navigating not just quarterly earnings and equity indices, but the Strait of Hormuz, tech tariffs, and capital flows chasing the next strategic alliance.

L’introduzione massiccia dell’Intelligenza Artificiale (IA) nel tessuto economico sta ridefinendo il mondo del lavoro. Nei prossimi 5-10 anni (indicativamente entro il 2030-2035), in particolare in Europa e Nord America, assisteremo a cambiamenti significativi: alcuni lavori verranno sostituiti dall’IA, altri verranno integrati con strumenti IA, emergeranno nuove professioni, e si osserverà un forte ricambio tra posti persi e creati. Questo report analizza in dettaglio tali aspetti, i flussi economici legati all’IA, le implicazioni socio-politiche, e propone strategie per una transizione equilibrata. I dati citati si concentrano soprattutto sul contesto occidentale, con uno sguardo alle tendenze globali.

1. Lavori che verranno sostituiti dall’IA

Non tutte le professioni sopravvivranno indenni alla rivoluzione dell’IA. I progressi nell’automazione mettono a rischio in particolare i lavori ripetitivi, manuali o basati su compiti routinari e dati strutturati, che risultano più facilmente automatizzabili. Studi recenti stimano che entro i prossimi 10 anni fino al 25-30% dei posti di lavoro complessivi potrebbe essere automatizzabile nei paesi avanzati, anche se l’impatto varia notevolmente da settore a settore. La tabella seguente riassume alcune previsioni di percentuale di sostituzione da parte dell’IA per settore, con relative tempistiche e fattori chiave:

Data entry, segreteria, contabilità di base automatizzabili tramite software IA (weforum.org)

Esempi concreti:

Nel manifatturiero, l’adozione di robot e sistemi di visione artificiale sta già sostituendo operai in catena di montaggio. Si prevede che fino al 44% dei posti produttivi potrebbe essere automatizzato entro metà anni ’30. Uno studio stima la perdita di 20 milioni di posti manifatturieri nel mondo entro il 2030 dovuta ai robot (resumeble.com). Le attività maggiormente a rischio includono assemblaggio, saldatura e controllo qualità ripetitivo.

Nei trasporti, i camion e taxi a guida autonoma potrebbero ridurre drasticamente la domanda di autisti: il settore dei trasporti è indicato come quello col più alto potenziale di automazione nel lungo termine (pwc.com) . Man mano che i veicoli autonomi diverranno economicamente e normativamente viabili, gran parte dei conducenti umani potrebbe essere sostituita (indicativamente fino a ~50% entro il 2035). Anche la logistica di magazzino è in automazione avanzata: ad es. Amazon impiega già oltre 500.000 robot magazzinieri per picking e smistamento (brandvm.com), migliorando la produttività ~20% (brandvm.com) e riducendo la necessità di magazzinieri umani.

Nel settore finanziario, molte mansioni sono altamente digitalizzabili: ad esempio, i sistemi IA analizzano contratti in pochi secondi sostituendo centinaia di ore di lavoro legale/amministrativo (brandvm.com). Le banche adottano robo-advisor e chatbot per le operazioni standard. Studi PwC evidenziano che settori basati sui dati come finanza e assicurazioni sono fortemente esposti all’automazione man mano che gli algoritmi superano le prestazioni umane in sempre più compiti analitici (pwc.com) . Questo potrebbe tradursi in circa un terzo dei ruoli attuali automatizzabili entro gli anni 2030.

Nel retail (commercio al dettaglio), l’impatto varia: le casse tradizionali e i commessi addetti a transazioni semplici sono in diminuzione a favore di soluzioni self-service e acquisti online. Già entro il 2024, circa 64% dei retailer mondiali ha introdotto casse self-service IA (brandvm.com), riducendo il bisogno di cassieri. Di conseguenza, ruoli come cassiere e addetto alle vendite di routine sono stimati in calo ~25% nei prossimi anni (hackernoon.com). Tuttavia, nel retail rimangono importanti attività umane come l’assistenza personalizzata, il merchandising creativo e la gestione di eccezioni (clienti difficili, prodotti difettosi), dove le macchine non eccellono ancora (brandvm.com)

Nei servizi amministrativi, di segreteria e data entry, l’IA sta avendo un effetto particolarmente forte. Compiti ripetitivi d’ufficio (inserimento dati, archiviazione, preparazione di documenti standard) possono essere svolti da software di automazione robotica dei processi (RPA) e agenti conversazionali. Il World Economic Forum prevede un rapido declino di queste figure: ad esempio i data entry clerks risultano tra i ruoli a più veloce contrazione a livello globale (weforum.org) [già -30% osservato di recente (hackernoon.com)]. Anche i cassieri di banca, addetti allo sportello e segretarie rientrano nei top 10 lavori in via di estinzione a causa dell’IA (weforum.org).

Fattori che determinano la sostituzione: Va sottolineato che l’automatizzabilità tecnica non implica automaticamente la sostituzione effettiva di quel lavoro (pwc.com). Diversi fattori influenzeranno la velocità e portata della sostituzione:

Fattori economici: se il costo di implementazione dell’IA/robot è inferiore al costo del lavoro umano, l’incentivo all’automazione cresce. In settori con manodopera costosa (es. manifattura in paesi avanzati, logistica) l’adozione è più rapida (mckinsey.com). Al contrario, in contesti di lavoro umano a basso costo, l’automazione può essere meno prioritaria. Tuttavia, anche in paesi a basso salario, motivazioni come migliorare la qualità, la scalabilità e la vicinanza al mercato finale possono spingere verso l’IA (mckinsey.com).

Fattori tecnici: la maturità della tecnologia è cruciale. Alcune automazioni (es. veicoli completamente autonomi su strada pubblica) potrebbero richiedere più tempo del previsto per raggiungere affidabilità e sicurezza adeguate. L’“ondata di autonomia” completa è attesa negli anni ’30 proprio perché tecnologie come robotica avanzata e guida autonoma saranno pienamente mature solo allora (pwc.com).

Fattori normativi e sociali: normative sulla sicurezza, responsabilità e accettazione pubblica possono rallentare la sostituzione in certi settori. Ad esempio, l’impiego di AI mediche o veicoli autonomi richiede cornici regolatorie e fiducia dell’utenza. Inoltre, pressioni politiche per la tutela dell’occupazione possono incentivare misure che moderano l’automazione “selvaggia” (come proposte di tassare i robot o imporre quote minime di personale umano).

Limiti organizzativi: l’integrazione di nuove tecnologie richiede a volte la riorganizzazione dei processi aziendali e competenze nuove. Aziende poco pronte al cambiamento o con workforce non formata potrebbero posticipare l’adozione di IA, nonostante la fattibilità tecnica. Un sondaggio globale PwC ha rivelato che il 37% dei lavoratori teme di perdere il posto a causa dell’automazione (pwc.com) – tale percezione può spingere le imprese più lungimiranti a introdurre l’IA in modo graduale e socialmente responsabile per evitare contraccolpi.

In sintesi, molti lavori routinari e ripetitivi nei settori sopra elencati vedranno una significativa automazione (30-50% entro il 2030 in diversi ambiti). Tuttavia, la velocità di questo processo dipenderà da costi, sviluppo tecnologico e risposte normative. Rimarranno spazi per il lavoro umano laddove servono creatività, empatia, flessibilità e supervisione.

2. Lavori che verranno integrati con l’IA (complementarietà uomo-macchina)

In numerose professioni l’IA non rimpiazzerà completamente l’essere umano, ma diventerà un alleato indispensabile, trasformando la natura del lavoro. Si parla in questi casi di integrazione uomo-IA o “intelligenza aumentata”, dove la tecnologia assume compiti di supporto, velocizzando le attività e lasciando agli umani le decisioni critiche, la creatività e le relazioni interpersonali.

Esempi di integrazione per settore:

Sanità: invece di sostituire medici e infermieri, l’IA funge da strumento diagnostico e di supporto alle decisioni cliniche. Un esempio è la radiologia: algoritmi di visione artificiale possono individuare anomalie in immagini medicali con un’accuratezza 11,5% superiore a quella dei radiologi in alcuni casi (brandvm.com), evidenziando aree sospette. Ciò non elimina la figura del radiologo, ma la potenzia – il medico sfrutta i risultati dell’IA per concentrarsi sulle diagnosi più complesse e sul rapporto col paziente (brandvm.com). Allo stesso modo, sistemi IA analizzano i sintomi dei pazienti (es. chatbot medici, triage automatizzato) e possono ridurre del 25% le visite inutili dal dottore (brandvm.com), permettendo ai medici di dedicare più tempo ai casi seri. In sintesi, nel prossimo decennio vedremo chirurghi assistiti da robot, medici di base supportati da IA diagnostiche e infermieri aumentati da sensori e predizione di rischi – l’elemento umano rimarrà centrale per empatia, giudizio etico e decisioni personalizzate, mentre l’IA svolgerà calcoli e analisi veloci (brandvm.com,brandvm.com).

Educazione: anche se i tutor IA personalizzati diventeranno comuni, non rimpiazzeranno gli insegnanti umani bensì li affiancheranno. Software di apprendimento adattivo possono seguire i progressi di ogni studente, proporre esercizi su misura e persino correggere compiti meccanici, liberando i docenti da una parte del carico ripetitivo (brandvm.com). Ad esempio, sistemi di tutoring intelligente identificano le lacune di uno studente e suggeriscono esercizi mirati, permettendo al professore di impiegare il tempo in attività ad alto valore aggiunto (mentoring, progetti creativi, dialogo educativo) (brandvm.com). È improbabile che l’IA possa replicare appieno il ruolo motivazionale ed emotivo di un bravo insegnante – caratteristiche come leadership in classe, ispirare gli studenti e adattarsi alle dinamiche sociali restano prerogative umane. Pertanto, la scuola del futuro vedrà insegnanti potenziati dall’IA: meno tempo speso in burocrazia e correzioni, più tempo in creatività e supporto personale. I sistemi educativi occidentali stanno già adattandosi: molte scuole e piattaforme (Coursera, edX) introducono corsi su competenze digitali e IA per preparare studenti e lavoratori al futuro (brandvm.com).

Servizi alla clientela (customer service, hospitality): qui l’IA (soprattutto chatbot e assistenti virtuali) sta trasformando il modo di interagire con i clienti, ma tipicamente non elimina del tutto l’operatore umano, piuttosto filtra e semplifica il suo lavoro. Ad esempio, assistenti virtuali rispondono 24/7 a domande frequenti su siti web bancari o e-commerce; un caso è Erica di Bank of America, chatbot che ha già gestito 100 milioni di richieste dei clienti in modo automatico (brandvm.com). Ciò riduce il carico sul call center tradizionale. Secondo analisi di settore, entro il 2025 i bot AI potrebbero gestire fino al 95% delle interazioni cliente iniziali (masterofcode.com), inoltrando agli operatori umani solo i casi complessi. Questo significa che i ruoli di front-line (centralinisti, sportellisti) diminuiranno di numero, ma diventeranno più specializzati: l’addetto interviene come “escalation” per problemi che richiedono empatia, creatività o interventi discrezionali. In ambito alberghiero/ricettivo, già ora molti hotel usano chatbot per prenotazioni e informazioni di base (brandvm.com), oppure chioschi self-service per il check-in. Il personale umano però rimane fondamentale per gestire gli ospiti, risolvere imprevisti e offrire quel tocco personale che incide sulla soddisfazione. In definitiva, nei servizi ai clienti l’IA fungerà da “filtro intelligente”: eliminerà le code e velocizzerà le risposte semplici, mentre i lavoratori umani gestiranno meno interazioni totali ma di qualità/più complesse.

Produzione e manutenzione industriale: l’uso di robot collaborativi (“cobot”) in fabbrica consente agli operai specializzati di lavorare fianco a fianco con macchine intelligenti. Le linee produttive moderne non sono più “solo umane” né totalmente automatizzate, ma ibride. Ad esempio, nelle fabbriche Tesla i robot eseguono saldature e movimentazione materiale con estrema precisione, mentre gli umani si occupano di supervisione e compiti non standard: questo mix ha ridotto i costi di produzione di circa il 30% (brandvm.com). L’International Federation of Robotics (IFR) riporta che il mercato globale dei robot industriali ha raggiunto ~$18,2 miliardi nel 2023 con oltre 500.000 robot installati nel mondo (brandvm.com). In questo scenario, molte mansioni operative pure scompaiono, ma cresce il bisogno di tecnici di manutenzione, programmatori di robot e data analyst che mantengano ed ottimizzino tali sistemi (brandvm.com). Un indice interessante: le offerte di lavoro legate all’IA su LinkedIn sono aumentate del 60% annuo nel 2023 (brandvm.com) (segnando la domanda di competenze di integrazione). Questo riflette la trasformazione del lavoro in fabbrica: meno operai a svolgere mansioni manuali ripetitive, più specialisti che gestiscono le macchine, analizzano i dati di produzione e risolvono problemi tecnici brandvm.com. La presenza dell’IA in stabilimento, quindi, non elimina totalmente il fattore umano ma ne cambia il ruolo: dall’“esecutore” al “supervisore/risolutore di problemi”.

Finanza e legal (parte analitica): banche e studi legali adottano IA per elaborare grandi moli di dati – es. revisione automatica di contratti, rilevazione di frodi, trading algoritmico – ma mantengono personale esperto per l’interpretazione dei risultati e la gestione delle eccezioni. In una banca d’investimento moderna, l’IA può gestire oltre il 60% del volume di trading azionario (brandvm.com) e piattaforme come JPMorgan COIN analizzano migliaia di pagine di contratti in pochi secondi (brandvm.com). Tuttavia rimangono vitali ruoli umani in compliance, regolamentazione e consulenza personalizzata: ad esempio, robo-advisor come Betterment offrono investimenti automatizzati a basso costo, ma per pianificazioni finanziarie complesse o esigenze emotive (es. rassicurare clienti in panico di mercato) i consulenti in carne ed ossa restano insostituibili (brandvm.com). Così anche nel diritto, l’IA ricerca giurisprudenza e precedenti, ma gli avvocati umani costruiscono la strategia legale e persuadono in aula. Possiamo attenderci entro 5-10 anni uffici finanziari “ibridi”: un piccolo team umano amplificato da potenti strumenti IA sarà in grado di gestire portafogli e analisi che prima avrebbero richiesto decine di persone.

In generale, la tendenza è verso un modello di lavoro ibrido uomo-macchina. Secondo Accenture, il 65% del tempo oggi speso in attività lavorative basate sul linguaggio (es. leggere, scrivere, analizzare testi) potrà essere trasformato tramite automazione o augmented intelligence anziché essere completamente rimpiazzato (weforum.org). Ciò significa che, per una larga fetta di professioni, l’IA ridisegnerà il contenuto del lavoro senza eliminare il lavoratore: parte delle mansioni verranno delegate alle macchine e al software, mentre l’umano si focalizzerà su aspetti più strategici, creativi o di interazione sociale.

Va notato che questa integrazione, pur essendo positiva per la produttività, potrebbe impattare i livelli occupazionali: se una singola persona con l’ausilio dell’IA può svolgere il lavoro che prima richiedeva un intero team, è plausibile che le aziende riducano il numero di impiegati in certi reparti. Ad esempio, nel software development, un ingegnere supportato da strumenti di codifica automatica (come GitHub Copilot) può scrivere codice più velocemente, potenzialmente diminuendo la necessità di grandi team di programmatori su progetti standard. Goldman Sachs stima che le tecnologie di IA generativa potrebbero automatizzare mediamente il 25% delle mansioni in ogni lavoro nei paesi avanzati (nextbigfuture.com). Molti di questi compiti saranno “collaborativi” (eseguiti dall’IA con supervisione umana). Quindi, pur senza licenziamenti immediati, le nuove assunzioni potrebbero rallentare in alcuni settori integrati con l’IA, portando a una riduzione graduale dell’occupazione netta in ruoli dove un individuo aumentato dall’IA basta a coprire mansioni che prima richiedevano più persone.

In sintesi, nei prossimi 5-10 anni vedremo un’ampia adozione dell’IA come complemento al lavoro umano: l’uomo+macchina sarà il paradigma vincente in sanità, istruzione, finanza, manifattura avanzata e servizi. Ciò richiederà però ai lavoratori di riqualificarsi per sfruttare gli strumenti IA (ad esempio, i medici dovranno imparare a interpretare i referti prodotti dall’IA, gli insegnanti a usare le piattaforme di e-learning adattive, etc.). Le aziende più competitive saranno quelle che riusciranno a ridisegnare i processi attorno alla collaborazione uomo-IA e a formare adeguatamente il personale su queste nuove competenze (weforum.org).

3. Nuovi lavori creati dall’IA

Accanto ai fenomeni di distruzione e trasformazione del lavoro, l’Intelligenza Artificiale farà da volano per la creazione di nuove professioni e figure specializzate, molte delle quali difficilmente immaginabili solo pochi anni fa. La storia insegna che ogni rivoluzione tecnologica – dalla meccanizzazione industriale all’avvento del computer – ha generato occupazioni inedite (dall’operaio specializzato al programmatore). Analogamente, l’era dell’IA sta già creando ruoli emergenti, e nei prossimi 5-10 anni vedremo un’accelerazione di questo trend.

Figure professionali emergenti grazie all’IA:

Specialisti in Intelligenza Artificiale e Machine Learning: sono gli sviluppatori di algoritmi e gli ingegneri che progettano, addestrano e ottimizzano modelli IA. La domanda di questi profili è in forte crescita: il World Economic Forum prevede un aumento del 40% nel numero di esperti AI/ML entro il 2027 (weforum.org). Questi ruoli includono Machine Learning Engineer, Data Scientist, AI Researcher e simili. Già oggi compaiono posizioni come “Prompt Engineer” (esperto nel formulare input ottimali per sistemi IA generativi) o AI Solutions Architect. I dati LinkedIn confermano la tendenza: gli annunci per “artificial intelligence specialist” sono cresciuti dell’hype ai primi posti dei lavori emergenti in molte regioni del mondo. Questa categoria di nuovi lavori è richiesta non solo nel tech puro, ma in tutti i settori che integrano l’IA (dalle banche alla sanità), fungendo da “costruttori” delle soluzioni di IA interne.

Analisti di dati e Big Data specialist: l’IA genera e richiede enormi quantità di dati; servono quindi professionisti capaci di gestire, interpretare e ricavare insight da questi dati. Ruoli come Data Analyst, Data Scientist, Big Data Specialist vedranno una crescita del 30-35% nei prossimi 5 anni secondo il WEF (weforum.org). In effetti, con la diffusione dell’IA ogni azienda dovrà capire come usare i dati (clienti, operazioni, mercato) per migliorare prodotti e processi – aumentando la richiesta di esperti in statistica, analytics avanzato e visualizzazione dati. Accanto a loro, anche i Cloud computing specialists e gli ingegneri del software AI saranno molto richiesti, dato che le infrastrutture cloud e l’implementazione software sono alla base delle soluzioni di IA (il WEF stima +30% domanda per questi ruoli tech correlati) (weforum.org).

Specialisti in cybersecurity e AI security: con l’aumento di sistemi IA nelle operazioni critiche, cresce il bisogno di proteggere questi sistemi da attacchi o anomalie. Figure come Information Security Analyst e AI Security Specialist sono in ascesa – il WEF prevede un +31% di domanda entro il 2027 per analisti della sicurezza informatica (weforum.org). Inoltre emergeranno ruoli specializzati nella sicurezza dei modelli IA (assicurarsi che gli algoritmi non vengano manipolati, difendere dai cosiddetti adversarial attacks, garantire privacy dei dati utilizzati per l’addestramento, ecc.).

Data Labeler / Annotatori di dati: paradossalmente, la creazione di IA avanzate spesso richiede molto lavoro umano a monte per preparare i dati di addestramento. Nascono così schiere di “annotatori” che etichettano immagini, trascrivono audio, correggono output dell’IA, in modo da migliorare i modelli. Ad esempio, per sviluppare veicoli autonomi servono persone che “insegnino” ai sistemi a riconoscere segnali stradali e ostacoli nelle immagini (brandvm.com); nel retail online, annotatori aiutano l’IA a comprendere foto di prodotti e recensioni clienti (brandvm.com). Questi lavori possono essere entry-level e distribuiti globalmente (spesso tramite piattaforme online di crowdworking), e costituiscono una nuova categoria di impiego generata direttamente dal bisogno di addestrare l’IA. Molti di questi ruoli sono temporanei o di transizione (man mano che l’IA migliora, la necessità di annotazione manuale potrebbe calare), ma nell’orizzonte 2025 essi rappresentano un importante bacino di impiego (si pensi ai “turk” di Amazon Mechanical Turk o ai team di annotazione di grandi aziende tech).

Esperti di integrazione e sviluppo business con IA: man mano che l’IA penetra in ogni settore, sono richiesti professionisti capaci di colmare il gap tra tecnologie IA e obiettivi di business. Ad esempio, gli AI Integration Specialists aiutano a implementare sistemi IA nei processi aziendali esistenti e a formare il personale all’uso (brandvm.com). Un report Deloitte indica che oltre il 45% delle grandi imprese ha assunto specialisti di integrazione AI già nel 2023 (brandvm.com). Allo stesso modo, ruoli come Digital Transformation Specialist e Innovation Manager stanno evolvendo per includere competenze specifiche di IA, con l’obiettivo di identificare nuove opportunità di mercato sfruttando l’intelligenza artificiale (prodotti data-driven, servizi personalizzati tramite AI, ecc.). Queste figure fungono da “ibridi” tra competenze tecniche e manageriali, e saranno cruciali per generare nuovo valore economico dall’IA (di conseguenza, rappresentano nuovi posti di lavoro qualificati).

Specialisti di etica, policy e governance dell’IA: l’adozione ubiqua dell’IA solleva dilemmi etici (bias algoritmici, privacy, impatti sociali) e richiede conformità a normative emergenti (come l’AI Act in UE). Sta dunque emergendo la figura dell’“AI Ethicist” o esperto di etica dell’IA, incaricato di guidare lo sviluppo e l’uso di algoritmi in maniera responsabile (onlinedegrees.sandiego.edu). Questi professionisti spesso hanno un background misto (tecnico e umanistico/giuridico) e aiutano le organizzazioni a implementare principi etici, audit di algoritmi e programmi di compliance. La domanda di esperti in etica/compliance AI è in forte crescita mano a mano che regolatori e aziende pongono attenzione al tema (onlinedegrees.sandiego.edu). Parallelamente, nei governi e nelle organizzazioni internazionali nascono ruoli dedicati a policy dell’IA – ad esempio, consulenti per la regolamentazione algoritmica, responsabili di governance dei dati, ecc. – che fino a pochi anni fa non esistevano. Anche le commissioni sul lavoro e gli enti di welfare potrebbero inserire specialisti per valutare l’impatto dell’automazione e formulare risposte di policy, configurando così un’altra area occupazionale indirettamente creata dall’IA.

Manutentori e tecnici di robotica/IA: con la proliferazione di macchine intelligenti e sistemi automatizzati, vi sarà crescente bisogno di personale tecnico che mantenga operativa questa infrastruttura. Già oggi si cercano robotics engineers, tecnici di assistenza per veicoli autonomi, specialisti nell’assistenza di strumenti medici AI-driven, ecc. (brandvm.com). Ogni nuova installazione di IA e robot genera filiere di supporto: ad esempio, l’introduzione di droni agricoli e trattori autonomi crea opportunità per tecnici agrari specializzati in elettronica e IA (una sorta di “meccatronico agricolo”). Nel settore IT, l’aumento di sistemi AI cloud-based crea domanda per MLOps engineers – figure che si occupano della messa in produzione e monitoraggio continuo dei modelli IA in azienda. Insomma, per ogni tecnologia intelligente diffusa su larga scala servirà una rete di competenze umane di supporto e manutenzione, un po’ come l’auto ha creato meccanici, benzinai, addetti alle infrastrutture stradali nel ‘900.

Professioni derivate dall’innovazione guidata dall’IA: non tutte le nuove professioni riguarderanno direttamente lo sviluppo o la gestione della tecnologia; molte saranno ruoli nati in settori abilitati dalla presenza dell’IA. Ad esempio, l’IA sta accelerando la scoperta di nuovi farmaci (drug discovery): di conseguenza, possono emergere nuovi ruoli biotecnologici specializzati nel collaborare con algoritmi per la ricerca farmaceutica. Oppure, nell’industria creativa, strumenti di generative AI (per immagini, video, musica) danno vita a figure come AI content creator o designer di esperienze virtuali che uniscono arte e tecnologia. Anche nel campo legale, potrebbe diffondersi lo “AI-assisted lawyer” che è un avvocato specializzato nell’uso di software di analisi legale (un ruolo a cavallo tra l’IT giuridico e la pratica legale). Nel marketing, già ora i professionisti devono saper utilizzare strumenti AI per l’analisi clienti e la personalizzazione: stanno nascendo ruoli di marketing technologist con forte componente AI. L’IA quindi funge da catalizzatore non solo di figure tecniche, ma anche di nuove nicchie professionali in settori tradizionali, ridefiniti da questi strumenti.

Quantificazione e peso dei nuovi lavori: Secondo il World Economic Forum, entro il 2027 le professioni emergenti legate a dati e IA cresceranno tanto da aggiungere 2,6 milioni di nuovi posti di lavoro a livello globale (tra AI specialist, data scientist, specialisti trasformazione digitale, ecc.) (weforum.org, weforum.org). Inoltre, si stima che circa il 8-9% della forza lavoro 2030 sarà impiegata in ruoli che oggi non esistono ancora (mckinsey.com), una buona parte dei quali legati direttamente o indirettamente all’IA. Questo tasso di creazione di nuove occupazioni è in linea con la storia tecnologica (negli anni 2010 sono emersi app economy, social media manager, specialisti cybersecurity, ecc.).

Un altro dato indicativo: ruoli tecnico-digitali (come big data, AI, cloud) figurano ai primi posti per tassi di crescita >50-100% anno su anno in diversi mercati del lavoro (hackernoon.com). Ad esempio, il numero di Big Data Specialists è raddoppiato in pochi anni (+100%) e gli specialisti di AI/ML sono aumentati dell’80% secondo analisi recenti (hackernoon.com). Questo trend suggerisce una forte domanda insoddisfatta, con ottime opportunità per chi si forma in tali campi.

In definitiva, l’IA non è solo un “distruttore” di posti di lavoro, ma anche un formidabile creatore di nuove professioni. Molti dei lavori del 2030-2035 ruoteranno attorno all’IA: progettandola, controllandola, applicandola nei vari contesti, o affrontando le sue implicazioni etiche e organizzative. La sfida sarà far sì che la forza lavoro attuale e futura possa riconvertirsi o formarsi adeguatamente per ricoprire questi nuovi ruoli.

4. Bilancio tra perdita e creazione di posti di lavoro

Un quesito cruciale è se l’IA finirà per creare più posti di quanti ne eliminerà, o viceversa, nel medio termine. La risposta non è semplice e dipende da molti fattori (scenario economico, velocità dell’innovazione, politiche adottate). Diversi studi forniscono stime quantitative sul bilancio tra job destruction e job creation dovuto all’IA e all’automazione.

Proiezioni chiave sul saldo occupazionale:

Il World Economic Forum (WEF) nel suo rapporto “Future of Jobs 2020” (pubblicato a fine 2020) prevedeva che entro il 2025 l’automazione avrebbe eliminato circa 85 milioni di posti di lavoro, ma creato circa 97 milioni di nuovi ruoli emergenti, con un saldo positivo di 12 milioni di posti (circa +5% rispetto al campione considerato) (weforum.org, weforum.org). In altri termini, in quella previsione ottimistica, i lavori creati dall’IA supererebbero quelli distrutti (~97M vs 85M). Questa stima teneva conto di 15 industrie in 26 economie avanzate/emergenti.

A pochi anni di distanza, il Future of Jobs Report 2023 del WEF ha rivisto il quadro, suggerendo maggiore cautela. Per il periodo 2023-2027 le aziende intervistate indicano di aspettarsi 69 milioni di nuovi posti creati contro 83 milioni di ruoli eliminati, con un saldo negativo di 14 milioni (circa -2% dell’occupazione totale analizzata) (hackernoon.com). In sostanza, nel prossimo quinquennio le perdite potrebbero eccedere i guadagni occupazionali, secondo questo sondaggio globale di aziende. Ciò rappresenta un cambiamento di prospettiva rispetto al report precedente, imputabile anche agli effetti accelerati della pandemia e dell’automazione correlata.

Nota: La % si riferisce alla quota di forza lavoro considerata nei campioni dei report.

La McKinsey Global Institute, in uno studio ampio del 2017, stimava che entro il 2030 tra 400 e 800 milioni di lavoratori nel mondo potrebbero essere dislocati dall’automazione (cioè costretti a cambiare occupazione) (mckinsey.com). Tuttavia, il medesimo studio concludeva che, con sufficiente crescita economica e innovazione, si creeranno abbastanza nuovi lavori da compensare quelli persi (mckinsey.com). In particolare, prevedeva che l’8-9% dei lavoratori al 2030 sarà impiegato in occupazioni nuove mai esistite prima (grazie alla tecnologia) (mckinsey.com), contribuendo a riassorbire molti degli esuberi da automazione. Lo scenario McKinsey ottimistico suggerisce quindi un equilibrio nel lungo periodo: i posti eliminati dall’IA sarebbero rimpiazzati da posti in nuovi settori, a condizione di investire in innovazione e riqualificazione dei lavoratori.

Analisi più recenti (2023) di Goldman Sachs hanno fatto molto scalpore affermando che l’IA generativa potrebbe impattare fino a 300 milioni di posti di lavoro a tempo pieno globalmente, specie in Nord America ed Europa (forbes.com). Ciò non significa disoccupazione di 300 milioni di persone, ma un significativo cambiamento nei contenuti lavorativi: in media il 25% delle mansioni di ogni lavoro potrebbe essere automatizzato (nextbigfuture.com). Goldman stima però che questa ondata tecnologica potrebbe aumentare la produttività a tal punto da far crescere il PIL globale di ~7% addizionale nel lungo termine (cnbc.com), il che storicamente tende a creare nuova occupazione in altri settori. In sostanza, Goldman prospetta un forte impatto trasformativo (un quarto del lavoro odierno svolto da macchine) ma con potenziali benefici macroeconomici che potrebbero generare nuovi lavori indirettamente, analogamente ad altre rivoluzioni tecnologiche.

OECD: studi come quello di Arntz et al. (OECD 2016) suggeriscono che mediamente solo ~14% dei posti attuali nei paesi OCSE è ad alto rischio di automazione completa (molto meno del 47% ipotizzato in uno studio Oxford 2013) poiché molte professioni hanno anche compiti difficilmente automatizzabili. Tuttavia, circa il 32% dei lavoratori potrebbe vedere cambiato significativamente il proprio lavoro dall’IA (mckinsey.com). L’OECD quindi vede più trasformazione dei ruoli che eliminazione netta totale, e sottolinea la necessità di aggiornare le competenze.

Complessivamente, il saldo tra posti persi e creati dall’IA è oggetto di dibattito e le stime variano: alcuni report indicano un leggero netto negativo nel breve termine (prossimi 5 anni), altri prevedono un possibile netto positivo o quantomeno un pareggio nel lungo termine (10+ anni), specialmente se si attuano politiche adeguate. È probabile che coesistano entrambe le dinamiche: inizialmente l’IA potrebbe sopprimere più posti di quanti ne generi (fase di disruption), mentre col tempo, grazie ai guadagni di produttività e alla creazione di interi nuovi settori, l’occupazione complessiva potrebbe recuperare o superare i livelli iniziali (fase di adjustment).

Va inoltre considerato il forte “churn” (ricambio) atteso: anche se il saldo netto fosse vicino allo zero, la composizione del lavoro sarà stravolta. Il WEF 2023 parla di un turnover del 23% dei lavori entro 5 anni (hackernoon.com), segno che quasi un lavoratore su quattro cambierà mansione o settore a causa di queste trasformazioni. Ciò rappresenta una sfida enorme in termini di transizioni di carriera: milioni di persone dovranno essere riqualificate o spostate da settori in declino a settori in crescita.

Occidente vs. globale: Nei paesi occidentali (Europa, Nord America) l’automazione avanzata e l’IA potrebbero inizialmente erodere più posti tradizionali (data la struttura economica ad alto costo del lavoro), ma al contempo queste regioni stanno guidando anche l’innovazione che crea nuovi lavori specializzati. Ad esempio, in Europa è atteso un calo in produzione manifatturiera tradizionale, ma una crescita in posti “verdi” e digitali; mentre negli USA alcuni analisti stimano che ~1/3 della forza lavoro potrebbe dover cambiare professione entro il 2030, ma con prospettive di piena occupazione se l’economia cresce e i lavoratori si aggiornano (mckinsey.com, mckinsey.com). A livello globale, paesi con popolazione giovane e in espansione (es. India, Sud-Est Asiatico) potrebbero continuare a vedere aumento netto dell’occupazione, poiché il balzo di produttività dell’IA può stimolare crescita economica e nuova domanda di lavoro (ad esempio la domanda di servizi e consumo aumenta con l’aumento di reddito generato dall’IA). Di contro, regioni che non riusciranno a innovare o formare la propria forza lavoro potrebbero subire di più gli effetti negativi (disoccupazione tecnologica).

In definitiva, l’IA eliminerà molti lavori, ma ne creerà altrettanti di nuovi – il bilancio finale dipenderà da come governi e imprese gestiranno la transizione. Le stime quantitative mostrano scenari sia positivi sia negativi: possiamo aspettarci anni di intensa distruzione creatrice (per dirla con Schumpeter), con un periodo di transizione turbolento in cui coesisteranno disoccupazione settoriale e carenza di competenze in nuovi ruoli. La chiave sarà accompagnare la forza lavoro nei settori emergenti per far sì che i posti creati superino quelli persi nel lungo termine.

5. Flussi economici legati all’IA: investimenti, mercato e impatti finanziari

L’Intelligenza Artificiale non è solo una forza lavoro, ma anche un settore economico in rapidissima crescita. Si prevede che nei prossimi 5-10 anni l’IA diventi uno dei principali driver di investimenti e crescita del PIL a livello globale. Di seguito analizziamo i principali flussi economici collegati all’IA: il giro d’affari del mercato IA, gli investimenti previsti (pubblici e privati), la crescita di mercato e gli impatti macroeconomici attesi.

Dimensioni del mercato globale dell’IA: Il mercato dell’IA comprende software, hardware e servizi legati a sistemi di intelligenza artificiale. Nel 2023 il mercato globale dell’IA è stimato intorno ai $200 miliardi di dollari (faistgroup.com). Le proiezioni indicano una crescita esponenziale entro la fine del decennio: a tassi composti annui superiori al 35%, il mercato potrebbe superare i $1.8 trilioni (1.800 miliardi) nel 2030 (faistgroup.com). In altre parole, si tratta di un settore destinato a moltiplicarsi di quasi 10 volte in meno di 10 anni. Secondo Statista, il volume d’affari IA potrebbe oltrepassare già gli $800 miliardi nel 2030 come stima conservativa (statista.com), mentre analisi più ottimistiche come Grand View Research citano addirittura $1.8 trilioni (faistgroup.com). Questa differenza di stime dipende dalle definizioni (cosa si include esattamente nel “mercato IA”). In ogni caso, l’IA rappresenta uno dei mercati a più rapida espansione nella storia moderna, paragonabile al boom di Internet negli anni ’90 in termini di crescita percentuale.

Investimenti e spesa in IA: Gli investimenti privati in IA (aziendali e venture capital) hanno conosciuto un vero boom. Nel 2013 gli investimenti corporate globali in IA ammontavano a circa $14,6 miliardi, mentre nel 2023 hanno raggiunto circa $189 miliardi (wisdomtree.com) – una crescita di ben 13 volte in un decennio. Questo trend riflette la corsa di aziende grandi e piccole ad adottare l’IA per non restare indietro. Anche il finanziamento delle startup IA è aumentato vertiginosamente: solo nel settore dell’IA generativa, nel 2023 si sono investiti circa $25 miliardi di VC, quasi 9 volte l’anno precedente (aiindex.stanford.edu, aiindex.stanford.edu), sulla scia del successo di modelli come ChatGPT. Va menzionato che dopo un picco nel 2021, gli investimenti totali in IA hanno avuto una leggera frenata nel 2022 (in linea col raffreddamento dei mercati tech), ma il boom dell’IA generativa nel 2023 ha riacceso la crescita (aiindex.stanford.edu).

Le grandi aziende tech (FAANG, Microsoft, etc.) stanno dirottando budget enormi verso l’IA: ad esempio, Microsoft ha investito miliardi in OpenAI; Google/Alphabet spende oltre $AI in ricerca annualmente. Anche i governi occidentali sono attivi: l’UE ha annunciato piani di investimento da miliardi di euro per ricerca e sviluppo in AI (es. programma Horizon Europe), e gli USA tramite DARPA e NSF stanno finanziando centri di eccellenza sull’IA. In Asia, la Cina (pur fuori dal focus occidentale principale di questo report) investe massicciamente in IA con piani governativi dedicati.

Crescita per settori: Alcuni settori trainano la spesa in IA: media e advertising, sanità, bancario/assicurativo (BFSI) sono ad oggi i maggiori acquirenti di soluzioni IA (faistgroup.com, faistgroup.com). Nel 2023, il comparto advertising & marketing è risultato il primo segmento per fatturato IA (grazie alla pubblicità online mirata e all’analisi dati clienti), e si prevede rimarrà tra i più dinamici fino al 2030 (faistgroup.com). La sanità è un altro campo con enorme potenziale: l’adozione di IA per diagnosi, scoperta farmaci, gestione cartelle cliniche sta crescendo con CAGR altissimi. La finanza è già da tempo in prima linea (trading algoritmico, prevenzione frodi, robo-advisor). Il manifatturiero vedrà aumentare la spesa in IA soprattutto per automazione di fabbrica e manutenzione predittiva. Anche automotive (veicoli autonomi, smart features) e retail (personalizzazione, supply chain intelligente) avranno quote significative di investimento IA. In sintesi, quasi ogni settore sta incrementando le proprie spese in intelligenza artificiale, con priorità diverse a seconda dei casi d’uso (es. l’automotive sull’hardware/sensori, il software sul cloud, il retail sui recommendation engines, ecc.).

Impatto economico macro (PIL e produttività): L’IA è vista come un motore di produttività e crescita economica paragonabile alle grandi innovazioni del passato (motore a vapore, elettricità, IT). PwC ha stimato che l’IA potrebbe aggiungere fino a $15,7 trilioni all’economia mondiale entro il 2030 (pwc.com) – effetto cumulato di maggiore produttività e aumento della domanda [per contestualizzare, $15 trilioni è più del PIL attuale di Cina e India messe insieme (pwc.com)]. Un’analisi del McKinsey Global Institute parlava di $13 trilioni di contributo al PIL globale al 2030 grazie all’IA (brandvm.com).

In termini di produttività, uno studio di Goldman Sachs calcola che l’adozione diffusa dell’IA generativa potrebbe innalzare la crescita annua della produttività negli USA di circa 1,5 punti percentuali per il prossimo decennio (gspublishing.com). Questo è un boost enorme, considerando che negli ultimi anni la produttività avanzava a meno del 1-2% annuo nei paesi sviluppati. Globalmente, ciò si tradurrebbe in un PIL mondiale più alto di circa +7% rispetto al trend di qui a 10 anni (cnbc.com).

Altri indicatori finanziari:

Secondo IDC, la spesa mondiale in sistemi di AI (includendo hardware, software e servizi) era ~$154 miliardi nel 2023 e crescerà anch’essa oltre $300 mld entro 2026 mckinsey.com , con una quota crescente di spesa dedicata specificamente all’IA generativa (che entro il 2026 rappresenterà ~1/3 del totale spesa AI).

Il ritorno sugli investimenti in IA appare significativo per le imprese: ad esempio, case study indicano riduzioni di costi del 20-30% e aumenti di ricavi per chi adotta soluzioni AI in settori come produzione e marketing (brandvm.com, brandvm.com). Ciò spinge ulteriormente nuove imprese a investire in IA, creando un circolo virtuoso di investimenti.

Il valore di mercato delle aziende leader nell’IA è in forte crescita: società specializzate in AI (es. Nvidia nei chip AI, OpenAI, start-up di computer vision, ecc.) hanno visto valutazioni in borsa o venture skyrockettare. Questo attira ancora più capitali finanziari nel settore (fondi di venture capital, private equity, ecc. focalizzati sull’IA sono in aumento).

Geografia degli investimenti: Attualmente, Stati Uniti e Cina dominano la scena dell’IA in termini di investimenti e asset. Gli USA rappresentavano ~50%+ degli investimenti privati globali in IA negli ultimi anni, con la Silicon Valley e altri hub (Boston, New York, Seattle) a fare da traino (statista.com). La Cina ha il supporto statale e colossi come Baidu, Tencent, Alibaba investendo molto, anche se i dati indicano investimenti privati attorno a $7-8 miliardi recentemente (secondo Statista: statista.com), inferiori agli USA ma comunque significativi. Europa sta aumentando gli investimenti ma è indietro: ad esempio, l’investimento privato totale in IA in Europa era stimato sotto i $20 miliardi, frammentato tra vari paesi. L’Unione Europea sta cercando di recuperare col varo di fondi comuni e incentivi, puntando anche su collaborazioni pubblico-private. Canada e UK sono altri poli attivi nell’IA (grazie a un forte ecosistema di ricerca, soprattutto in Canada per il deep learning con figure come Yoshua Bengio). Nel complesso, l’Occidente (USA/Europa) è leader nello sviluppo IA e attira gran parte dei capitali globali, anche se la competizione con la Cina è strategica e crescente.

Effetti finanziari e di mercato degni di nota:

Il boom dell’IA sta trainando interi mercati azionari: ad esempio, nel 2023 il titolo Nvidia (produttore di GPU usate nell’AI) ha superato $1 trilione di capitalizzazione di mercato grazie alla domanda esplosiva di chip IA. Anche altre società legate all’IA hanno visto rialzi notevoli. Questo crea una “corsa all’oro” in borsa sulle aziende percepite come vincenti nell’AI, il che a sua volta facilita loro raccogliere capitali per investire ancora (es. quotazioni di startup AI).

Le fusioni e acquisizioni nel settore AI sono in fermento: i giganti tech stanno acquisendo startup IA promettenti a valutazioni elevate per assicurarsi talenti e proprietà intellettuale. Questo flusso di M&A genera movimenti di miliardi (e opportunità di guadagno per investitori e fondatori).

C’è una crescente attenzione a come l’IA impatta i modelli di business e i rendimenti. Molte aziende tradizionali stanno segnalando agli investitori risparmi di costo ottenuti con automazione IA (ad esempio, UPS ha risparmiato 10 milioni di galloni di carburante l’anno con IA di ottimizzazione percorsi brandvm.com , traducendosi in minori spese operative). Tali efficienze migliorano i margini di profitto, aspetto seguito dai mercati finanziari.

D’altro canto, si discute di possibili impatti negativi: se l’IA porterà disoccupazione o riduzione di salari in alcuni settori, ciò potrebbe ridurre la domanda di consumo aggregata, con effetti recessivi locali. Inoltre, c’è il tema di una possibile maggiore concentrazione di ricchezza: le aziende in grado di sfruttare l’IA potrebbero aumentare i profitti a spese di competitor che escono dal mercato, accentuando il potere di pochi attori (fenomeno “winner-takes-all”). Questo aspetto economico-sociale sarà discusso nel punto successivo sulle implicazioni.

In sintesi, i flussi economici legati all’IA mostrano una forte crescita del mercato e degli investimenti. L’IA è destinata a diventare uno dei settori più remunerativi e con maggiore impatto sul PIL globale nel prossimo decennio. Di seguito riassumiamo alcuni dati chiave in forma tabellare:

Legenda: “trilione”= mille miliardi. Il tasso di adozione e le previsioni occupazionali delle imprese sono tratte dal sondaggio WEF 2023.

Dalla tabella e analisi, è evidente che l’IA muove già centinaia di miliardi di dollari e ha un potenziale di creare valore economico misurabile in decine di trilioni nei prossimi dieci anni. Questo boom economico è accompagnato però da sfide di redistribuzione e sostenibilità che affronteremo di seguito.

6. Implicazioni economiche, sociali e politiche dell’IA

L’impatto dell’IA sul lavoro non si limita all’economia e alle aziende, ma ha ampie implicazioni sul tessuto sociale e politico. Trasformazioni occupazionali su vasta scala, come quelle discusse, influenzano la distribuzione del reddito, le disuguaglianze, il ruolo delle istituzioni formative e le politiche di welfare degli Stati. In questo capitolo analizziamo tali implicazioni in Occidente (Europa e Nord America in primis), tenendo conto anche di dinamiche globali.

Disuguaglianze e divisione del lavoro: Una preoccupazione centrale è che l’IA possa aumentare le disuguaglianze economiche. Ciò avviene su più livelli:

Disuguaglianza tra lavoratori qualificati e non: L’IA tende a sostituire compiti manuali e ripetitivi spesso svolti da lavoratori a basso reddito o con minori qualifiche, mentre crea opportunità per lavoratori altamente qualificati (ingegneri, manager digitali) spesso meglio remunerati. Questo potrebbe ampliare il divario salariale. Studi mostrano che i paesi/regioni con forza lavoro meno istruita hanno una percentuale maggiore di lavori automatizzabili (>40%), mentre economie con lavoratori più formati hanno rischio minore (~20-25%) (pwc.com, pwc.com). Ciò suggerisce il potenziale di un aumento del gap tra chi possiede competenze complementari all’IA e chi no. I lavoratori “low-skill” rischiano più facilmente la disoccupazione tecnologica o la riduzione di salario, mentre i “high-skill” vedono aumentare la domanda dei loro profili.

Polarizzazione del mercato del lavoro: L’IA potrebbe accentuare la scomparsa dei lavori di fascia media (routine sia manuali che cognitivi) – es. impiegato contabile, operaio generico – e la contemporanea crescita sia di lavori altamente qualificati sia di lavori manuali non automatizzabili (es. badanti, lavori creativi). Questo fenomeno di “job polarization” era già in atto con l’automazione informatica e potrebbe aggravarsi, svuotando ulteriormente il ceto medio occupazionale.

Disuguaglianze tra imprese: Le imprese che riusciranno ad adottare l’IA efficacemente vedranno aumentare produttività e profitti, acquisendo vantaggio competitivo. Aziende con risorse per investire in IA (tipicamente grandi multinazionali tech o manifatturiere) potrebbero conquistare fette di mercato a scapito di aziende più piccole o tradizionali, accentuando la concentrazione di mercato. Già oggi vediamo mega-corporation dominare settori digitali con ingenti utili. Ciò potrebbe tradursi in disuguaglianza nei profitti e quindi nel potere di fissazione dei salari (le aziende dominanti potrebbero mantenere bassi i salari in alcuni settori data la minore concorrenza per la manodopera).

Disuguaglianze regionali e globali: A livello geopolitico, i paesi leader in IA (USA, alcune nazioni europee, Cina) potrebbero vedere un boost economico, mentre paesi che basavano la loro competitività sul lavoro a basso costo rischiano di perdere commesse (se l’industria occidentale rimpatria la produzione grazie all’automazione). Ad esempio, nazioni in via di sviluppo con industrie tessili, call center, assemblaggio elettronica potrebbero essere bypassate dall’automazione nei paesi d’origine, minacciando il loro sviluppo. Questo è un serio rischio di approfondimento del divario Nord-Sud. D’altro canto, l’IA potrebbe offrire opportunità anche in paesi emergenti (es. India punta a diventare hub di servizi IA, l’Africa sta esplorando l’uso di IA in agricoltura). Molto dipenderà dall’accesso a istruzione e investimenti in quelle regioni.

Occupazione e coesione sociale: Un aumento consistente della disoccupazione tecnologica, anche temporanea, avrebbe effetti sociali importanti. La perdita del lavoro per individui di mezza età in settori in declino (es. operai, impiegati amministrativi) può portare a insicurezza economica, stress sociale, aumento della povertà se il sistema di welfare non riesce a tamponare. Regioni mono-industriali (la “Rust Belt” americana, alcune aree industriali europee) potrebbero rivivere dinamiche di declino economico e disagio sociale simili a quelle viste con la globalizzazione e la deindustrializzazione degli ultimi decenni, questa volta causate dall’automazione. Ciò potrebbe tradursi in malcontento politico: storicamente, fasi di rapido cambiamento tecnologico senza adeguata protezione sociale hanno alimentato movimenti di protesta, populismi e richiesta di cambiamenti politici radicali.

Regolamentazione dell’IA: I governi occidentali stanno iniziando a rispondere alla diffusione dell’IA con iniziative normative, in particolare per affrontare i rischi e garantire un uso etico e sicuro. L’Unione Europea è all’avanguardia con la proposta di AI Act, una legislazione che classificherà gli usi dell’IA per livello di rischio e imporrà obblighi (trasparenza, divieti per applicazioni ad alto rischio, ecc.) (weforum.org). Questo sul fronte tecnico/etico. Sul fronte lavoro, ci si interroga se servano nuove regolamentazioni del lavoro in era IA:

Aggiornare le normative su licenziamenti e ammortizzatori per tenere conto delle cause tecnologiche.

Introdurre l’idea di una “riduzione dell’orario di lavoro” per distribuire i benefici di produttività dell’IA (ad es. settimane lavorative più brevi a parità di salario, politica discussa in alcuni paesi).

Valutare misure come la tassazione dei robot o dell’IA: es. tassare l’uso di automi che sostituiscono lavoratori, per finanziare il welfare. Questa idea, sostenuta da alcuni (Bill Gates nel 2017 propose una “robot tax”), è controversa ma parte del dibattito politico in Europa.

Norme per la trasparenza algoritmica verso i lavoratori: se un’azienda usa IA per decidere turni, valutazioni o assunzioni, potrebbero servire diritti di spiegazione per i dipendenti (evitando discriminazioni nascoste).

Riforma dei sistemi pensionistici e contributivi: meno lavoratori umani potrebbero significare minor gettito contributivo; alcuni propongono che le aziende che automatizzano di più contribuiscano maggiormente ai fondi sociali.

Queste discussioni sono in corso. Politicamente, c’è una spinta a non frenare l’innovazione ma a guidarla responsabilmente. Negli USA il dibattito normativo è più agli inizi rispetto all’UE, ma anche lì si moltiplicano le audizioni in Congresso e i documenti di policy su IA e lavoro.

Sistemi educativi: L’istruzione è sia una soluzione sia un ambito impattato. Da un lato, come visto, l’IA può aiutare a personalizzare l’apprendimento (sezione 2), dall’altro il contenuto dell’istruzione va ripensato. Le scuole e università occidentali stanno iniziando a:

Enfatizzare STEM e competenze digitali: per preparare più sviluppatori, data scientist, ecc. che sono richiesti sul mercato. Ad esempio, introduzione del coding e basi di IA già nelle scuole secondarie, nuovi corsi universitari in AI, machine learning, robotica (è il caso di molte università europee e nordamericane negli ultimi 5 anni).

Formare su soft skill “a prova di AI”: creatività, pensiero critico, capacità comunicative, problem solving complesso, che sono competenze meno replicabili dalle macchine. I sistemi educativi progressisti (Finlandia, ad es.) stanno adattando i curricula per puntare di più su queste abilità trasversali.

Educazione continua: con lavori meno stabili, i lavoratori dovranno formarsi più volte nella vita. Questo richiede infrastrutture educative per adulti: corsi professionalizzanti brevi, certificazioni, e-learning flessibile. Stati e aziende in Occidente investono in programmi di reskilling/upskilling. Ad esempio, il governo UK ha lanciato un National Retraining Scheme per supportare transizioni di carriera (pwc.com). Aziende come Amazon, AT&T e altre hanno stanziato fondi per riqualificare i propri dipendenti automatizzabili verso ruoli tecnici. Tuttavia, la portata di queste iniziative va ampliata di molto per tenere il passo con il cambiamento tecnologico.

Accesso equo all’istruzione di qualità: se non gestito, il divario tecnologico può diventare divario educativo. Chi ha accesso a buone scuole e formazione IA avrà i lavori del futuro, chi no rischia di restare indietro. Ciò spinge i policymaker a rafforzare l’istruzione pubblica, ridurre i costi dell’università, e favorire l’ingresso di gruppi sotto-rappresentati (donne, minoranze) nelle materie tecnico-scientifiche per evitare nuove forme di disuguaglianza.

Welfare e protezione sociale: Fornire un adeguato welfare durante la transizione è fondamentale. I sistemi di sicurezza sociale dovranno adattarsi:

Possibile necessità di ammortizzatori universali per periodi di disoccupazione più frequenti. Alcuni economisti e tech leader sostengono l’idea di un Reddito di Base Universale (UBI) come rete di sicurezza se l’IA ridurrà drasticamente la domanda di lavoro umano. Il venture capitalist Vinod Khosla ad esempio ha affermato che l’IA potrà svolgere l’80% del lavoro in molti mestieri e che un UBI potrebbe diventare cruciale per garantire la stabilità sociale (businessinsider.com, businessinsider.com). Personaggi come Elon Musk e Sam Altman (OpenAI) hanno espresso posizioni simili (businessinsider.com). Un reddito di base fornirebbe un sostegno minimo a tutti i cittadini, sganciato dal lavoro, riducendo l’impatto di disoccupazione tecnologica e permettendo alle persone di riqualificarsi o perseguire lavori creativi senza rischio di indigenza. Al momento, esperimenti UBI sono stati localizzati (Finlandia, Canada, alcuni stati USA) ma nessun grande paese l’ha adottato in pieno; tuttavia il dibattito sta entrando nel mainstream politico in Occidente, alimentato proprio dalle prospettive dell’automazione.

Rafforzare i sussidi di disoccupazione e la formazione: in alternativa o aggiunta all’UBI, molti esperti propongono di migliorare i sistemi attuali: indennità di disoccupazione più generose e legate a programmi di riqualificazione, incentivi alle aziende che riassorbono lavoratori di settori in crisi, crediti di imposta per chi investe in formazione del personale invece di licenziare. Ad esempio, potrebbe essere utile un “assicurazione di transizione” in cui un lavoratore automatizzato riceve non solo un sussidio ma anche formazione pagata dallo Stato/azienda per un nuovo ruolo.

Riconsiderare la relazione lavoro-reddito: se in futuro una parte significativa della popolazione non avrà un impiego tradizionale a tempo pieno (scenario estremo ma ipotizzato da alcuni futurologi), si dovranno trovare modalità di distribuzione della ricchezza generate dall’IA. Oltre al UBI, si discute di modelli come imposta negativa sul reddito, lavori garantiti dallo Stato (in settori dove c’è bisogno, es. cura ambientale, assistenza agli anziani) per assorbire chi è disoccupato, o di far sì che i benefici dell’aumento di produttività si traducano in riduzione dell’orario di lavoro per tutti (es. 4 giorni lavorativi a settimana). Queste sono scelte politiche e sociali di ampia portata.

Sistema pensionistico: con carriere più frammentate, potrebbe diventare necessario un sistema pensionistico più flessibile, portabile e integrativo, perché meno persone faranno 40 anni di contribuzione lineare. Ad esempio, pensioni finanziate dalla fiscalità generale o con contributi anche dei robot (come evocativo “fondo pensione alimentato dai robot”).

Stabilità politica: Politicamente, l’IA e il suo impatto sul lavoro potrebbero diventare temi di forte rilevanza elettorale. Partiti e movimenti potrebbero capitalizzare la paura della disoccupazione o, viceversa, promettere ricchezza e tempo libero grazie all’IA. È plausibile la nascita di richieste di regolamentazione protezionistica (ad esempio, limitare l’automazione in alcuni settori per salvare posti di lavoro, analogamente a come si invocano dazi per proteggere industrie domestiche). Ciò mette i decisori di fronte a un delicato equilibrio: abbracciare l’innovazione per i benefici macro, ma gestirne i costi sociali per evitare instabilità. Nei paesi occidentali con processi democratici, questo tema potrebbe ridefinire le tradizionali divisioni politiche: più che destra vs sinistra, potremmo vedere “progressisti tecnologi” vs “neo-luddisti o protezionisti del lavoro umano”. In realtà, finora c’è un consenso abbastanza trasversale sulla necessità di accompagnare il cambiamento con formazione e welfare, piuttosto che bloccarlo del tutto.

Cultura e società: Su un piano più generale, se l’IA assume compiti e decisioni, cambierà anche la percezione del lavoro nella società. Si potrebbero affermare nuove etichette sociali – per esempio, come verrà percepita una persona che non lavora perché il suo mestiere è stato automatizzato e riceve un sussidio? È una dinamica da tenere in conto per mantenere la dignità e il ruolo sociale degli individui anche al di fuori del lavoro tradizionale. Inoltre, con più tempo libero (in teoria) potrebbero crescere settori come volontariato, arti, cura della comunità – aspetti positivi se incoraggiati.